China: a giant of stone or salt?

A global power or a colossus with feet of clay – the anatomy of a power under strain

The world’s second-largest economy. The world’s leading manufacturing power. And yet, structurally shackled to the financial architecture of its rival.

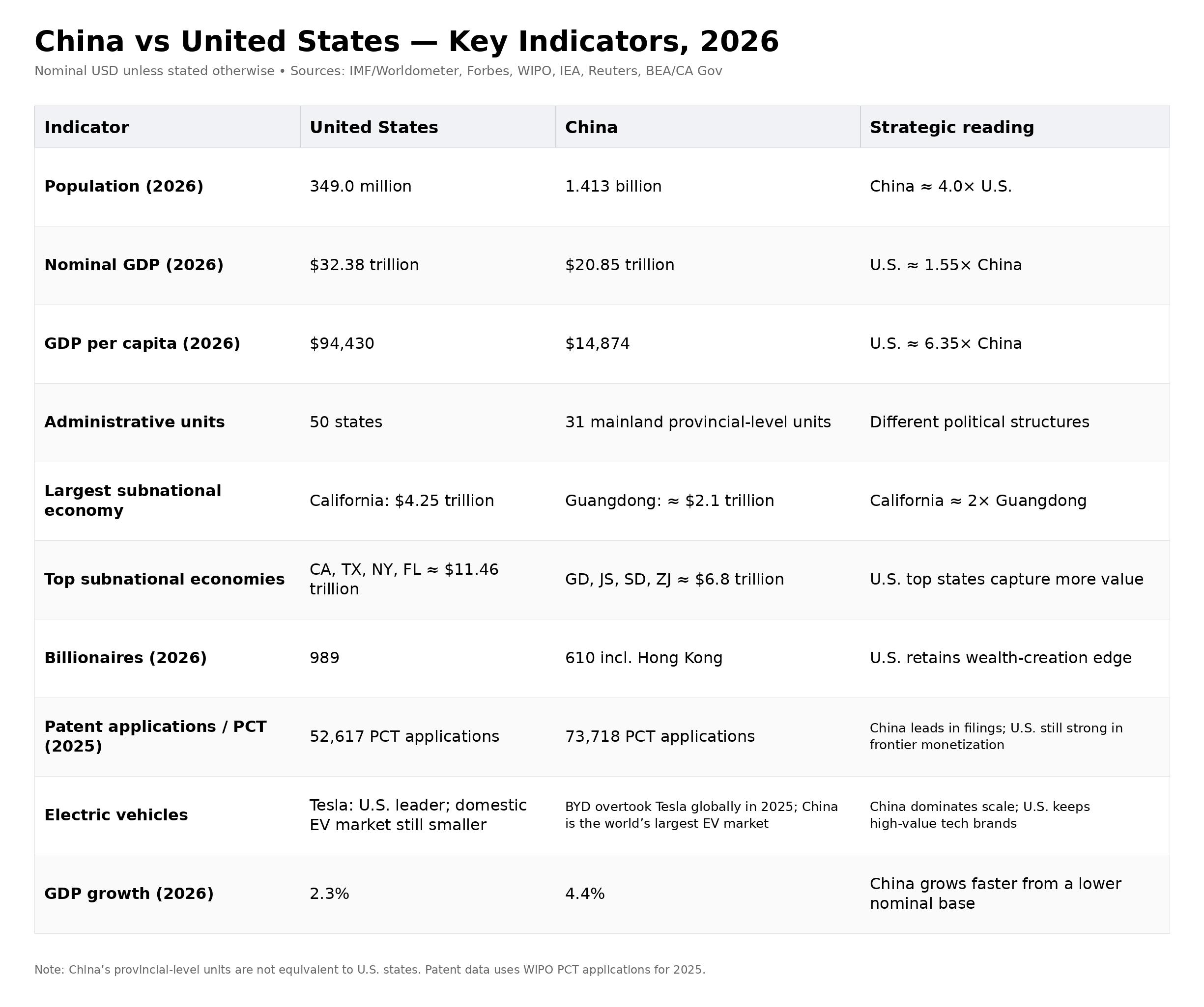

By 2025, the Chinese economy had surpassed the $20 trillion mark in nominal GDP. In 2026, the Chinese economy is estimated to be around $20.85 trillion in nominal GDP, according to IMF projections. With 4.4% annual growth, it remains one of the major drivers of global growth. Its manufacturing output exceeds that of the next nine countries combined. And yet, China has never seemed so vulnerable. A property crisis, deflation, an ageing population, hidden debt – and above all, an asymmetrical dependence on the dollar system that increasingly resembles an invisible leash. Following our analysis of the US foundation, the GAFAM , here is its systemic rival. A cornerstone of its industrial architecture. The salt in its financial foundations. Anatomy of a power under strain.

PART I The cornerstone: what makes China unshakeable

The strategic state. Where the United States operates through private competition, and Europe regulates without building, China has invented a hybrid model: state capitalism steered by the Communist Party through five-year plans. Nearly 867,000 Chinese companies have some degree of state ownership. SOEs — State-Owned Enterprises — account for a major share of the country’s largest listed companies. This integration between the state, public banks, industry and innovation has no equivalent in an economy of this scale.

The world’s factory. China manufactures more than the next nine manufacturing nations combined. Industry accounts for more than one-third of Chinese GDP, compared with less than one-fifth in the United States. In 2025, its trade surplus reached a historic high, at around $1.2 trillion according to available estimates. Steel, solar panels, batteries, electric cars, smartphones, household appliances: across dozens of critical value chains, China is no longer merely a supplier — it is an unavoidable passage point.

The complete digital ecosystem. Where GAFAM dominates everywhere except in China, Beijing has built its own internet: Baidu for search, Alibaba for e-commerce, Tencent and WeChat for social media and messaging, Huawei for telecoms infrastructure, ByteDance for content with TikTok and Douyin. It is the only digital space in the world that has managed to develop in parallel to the American model – under strict state control.

The stranglehold on critical minerals. China controls a decisive share of global supply chains linked to green energy and nearly 90% of rare earth refining. Not just extraction – above all, processing. Cobalt, lithium, rare earths, graphite, permanent magnets: without China, there would be no large-scale energy transition, no mass-produced batteries, no affordable solar panels, no industrial wind turbines and no critical components for semiconductors. If China is a cornerstone, it is because it possesses the material foundations of the global transition.

KEY FIGURES China in 2026

$20.85 trillion — estimated nominal GDP for 2026, making it the world’s second-largest economy.

Source: IMF / Worldometer, WEO data April 2026.

$44.3 trillion — estimated 2026 GDP at PPP, equivalent to approximately 44.3 trillion international dollars, the world’s largest economy at PPP.

Source: IMF / Worldometer, WEO April 2026.

4.4% — estimated real GDP growth for China in 2026.

Source: IMF / Worldometer, WEO April 2026.

2026 trade surplus under pressure — following a record of around $1.2 trillion in 2025, Reuters reports a sharp slowdown in March 2026 with a monthly surplus of $51.13 billion, well below expectations.

Source: Reuters.

60–85% — China’s share in several stages of clean energy technology production in 2026.

Source: IEA, Energy Technology Perspectives 2026.

91% — China’s share of global rare-earth magnet refining in 2024, according to the IEA; a key indicator still in 2026.

Source: IEA.

$693 billion — US Treasury bonds held by China in February 2026, down from a historic peak of $1,316.7 billion in November 2013.

Source: US Treasury / Trading Economics.

PART II The internal strain: domestic cracks

The property crisis. Property accounted for up to 30% of China’s GDP. The collapse of Evergrande, with around $300 billion in debt, followed by Country Garden and other developers, has exposed a hyper-leveraged financial system built on property speculation. Chinese households, which had invested most of their savings in property, have seen their wealth melt away. Confidence has collapsed. So has domestic consumption.

Deflation and the crisis of confidence. Unlike the rest of the world, which has been hit by post-Covid inflation, China has been experiencing persistent deflation since 2023. Households are saving rather than spending. Businesses are reluctant to invest. The parallel with Japan in the 1990s is illuminating, but imperfect: China retains an industrial depth, state leverage and outward reach that Japan did not possess to the same degree. But the risk is real: an economy that saves too much, consumes little, is ageing rapidly and is losing confidence may remain powerful whilst ceasing to catch up with its rival.

Youth under pressure. Youth unemployment, long at very high levels, has fuelled the phenomenon of tang ping – ‘lying flat’ – a form of silent withdrawal in the face of social competition deemed exhausting and unrewarding. This is not merely an economic problem. It is a psychological signal: when a generation doubts the promise of social mobility, a country’s internal engine begins to sputter.

Rapid ageing. China is ageing before it becomes rich. The one-child policy (1979–2015) created an unbalanced age pyramid. The working-age population has been declining since 2022. By 2050, nearly 40% of the Chinese population will be over 60. Beijing is attempting to address this through industrial robotisation, but robots compensate for the labour shortage without automatically stimulating domestic demand. No major economy has ever managed to sustain strong growth with such demographics.

The hidden debt of local authorities. Local Government Financing Vehicles (LGFVs) have accumulated debt estimated by the IMF at over $7 trillion – a high but credible estimate – equivalent to nearly 50% of GDP. This debt finances infrastructure that is sometimes unnecessary and remains largely opaque. A ticking time bomb that Beijing is attempting to defuse without causing panic.

PART III The American trap: China’s true vulnerability

This is probably the least understood aspect of China’s power. China is not financially independent from the United States: it remains trapped within the architecture of the dollar, US Treasuries and global trade.

The strategic error of 2008–2009. During the subprime crisis, whilst Washington was on the brink of collapse, Beijing bought up massive amounts of US debt. Over $1.3 trillion in Treasuries at the peak in November 2013. China thought it was gaining the upper hand over its rival, becoming its chief creditor. It was a trap. By buying so many dollars, Beijing tied its own hands: selling off large quantities would amount to devaluing its own reserves. Aware of the weakness of its strategy, it has revised its position, although it is still holding a substantial amount of over $693 billion as of February 2026.

The dollar’s leash. Beijing is reducing its Treasury holdings, buying gold, developing CIPS – China’s cross-border payment system designed to reduce dependence on the dollar/SWIFT architecture — and encouraging certain bilateral settlements in yuan. et despite these efforts, a significant share of its trade remains tied to the dollar/SWIFT system. The more China exports, the more it unwittingly finances the system it contests. IIt can challenge the American order; it still partially finances it. This is a self-reinforcing dependency.

Technological dependence. When it comes to advanced semiconductors, China remains dependent on ASML’s EUV lithography machines, which are subject to close strategic coordination with Washington. It is making rapid progress, but does not yet produce the most advanced chips on a large scale, as TSMC, Samsung or Intel do. When the US restricts access to the most powerful Nvidia chips or design software such as Cadence and Synopsys, Beijing’s progress slows.

The monetary stranglehold. International trade is still overwhelmingly settled in dollars. The yuan accounts for only a small share of global payments and reserves despite years of efforts to internationalise it. As long as this asymmetry persists, China remains structurally constrained. The dollar is a weapon. The yuan is still just a currency. They are not the same thing.

PART IV External projection and a power struggle

Faced with these vulnerabilities, Beijing is deploying an offensive strategy of circumvention.

Belt and Road Initiative: over $1 trillion committed across 150 countries – ports, railways, telecoms, energy. A commercial and geopolitical reach unmatched since the Marshall Plan.

BRICS+: with the expansion to include Iran, Saudi Arabia, Egypt and the UAE, the bloc now accounts for a major share of global GDP in PPP terms and over 45% of the world’s population. The digital yuan, bilateral agreements and partial de-dollarisation are making progress. But slowly. Too slowly to shake the dollar in the short term.

PART V Can China overtake the United States?

This is probably the most frequently asked question of the decade. The honest answer is twofold. Today: no, not in the indicators that matter. Tomorrow, looking 15–25 years ahead: yes, under strict conditions – that it restructures, innovates further, and loosens the grip of its dependence on the US.

Where China is already world number one. In terms of GDP at purchasing power parity, China is worth around $41 trillion internationally, compared with around $30 trillion for the United States. It dominates manufacturing, controls a major part of green supply chains, has become the world’s leading producer of electric vehicles by volume with BYD, the world’s leading battery manufacturer with CATL, the world’s leading producer of solar panels, a major player in 5G with Huawei, and a key player in rare earths. Its Belt and Road Initiative (New Silk Road) is making a commercial mark in 150 countries.

This is where the United States maintains a structural lead. In terms of nominal GDP, the gap remains considerable: nearly $30 trillion for Washington compared with around $20 trillion for Beijing. The dollar remains the global reserve currency. Wall Street remains unrivalled in terms of capital depth. Disruptive innovation continues to crystallise around Nvidia, OpenAI, Tesla, SpaceX, Anthropic and American biotech. Elite universities attract global talent. And the US’s global military reach is unrivalled.

The synthesis. China dominates in volume, the US in value. China produces, the US designs. China manufactures, the US captures the margins. PPP measures potential economic capacity; The real geopolitical balance of power is determined by nominal GDP, reserve currency status, breakthrough innovation and global military projection. Across these four dimensions, the gap remains substantial.

China has powerful champions – Huawei, BYD, CATL, ByteDance, DeepSeek – but still struggles to produce global standards as dominant as Nvidia in AI chips or OpenAI in the global technological imagination.

DeepSeek shows that Beijing can still surprise in AI, but within a framework where innovation remains aligned with political red lines. Its companies are brilliant, sometimes formidable, but caught between two constraints: innovating quickly and remaining compatible with the Party’s priorities. To understand what comes next, we must therefore not ask whether China is strong or weak. It is both at the same time. The real question is which force will prevail: the industrial discipline of stone, or the slow erosion of salt.

PART VI Three scenarios for China

Scenario 1 – Controlled consolidation. Beijing manages the property crisis without a collapse, gradually transitions to a domestic consumption model, maintains its manufacturing leadership and gains technological autonomy. China becomes a stable systemic rival to the United States without overtaking it in the short term.

Scenario 2 – Japanese-style stagnation. Persistent deflation, an ageing population, hidden debt, loss of domestic confidence. China enters a decade of sluggish growth. It remains powerful, but ceases to catch up with the United States. The parallel with Japan is imperfect, but useful: it is not collapse that threatens first, but stagnation.

Scenario 3 – Systemic breakdown. Major financial crisis, capital flight, a disengaged youth, persistent unemployment, political hardening. Low probability but not impossible. In this scenario, the Party retains control, but at the cost of permanently weakened growth.

Key Takeaways

China is not a monolithic bloc. It is a powerful system under pressure.

Stone in its industrial architecture and in its control of physical value chains.

Salt in its financial and demographic foundations, and in its asymmetric dependence on the American system.

The real question is not whether China will dominate the twenty-first century.

The real question is whether it can truly do so while remaining trapped within the architecture of the dollar. As long as the yuan remains more of a partial invoicing currency than a true global reserve currency, the leash is not made of rope, it is made of titanium.

→ In your view, can China truly free itself from its dependence on the dollar – or is that leash now too strong to be broken?

Intellectually yours,

Jean-Noël Niamké FINANCIAL EXPERT Economic, financial and geostrategic analysis

Sources: IMF, US Treasury TIC, Reuters, Chinese customs, IEA (critical minerals), IFR (robotisation), BBC (Tang Ping), Forbes, Bloomberg (consolidated data May 2026).